All Categories

Featured

Table of Contents

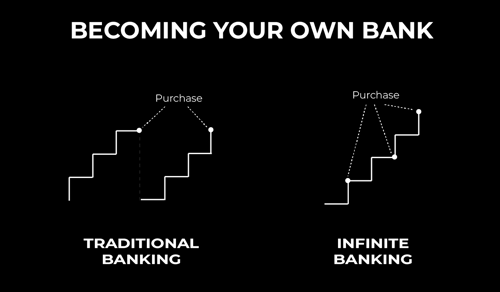

For many individuals, the most significant trouble with the limitless financial principle is that initial hit to very early liquidity caused by the costs. Although this disadvantage of infinite financial can be reduced significantly with proper plan style, the first years will constantly be the most awful years with any type of Whole Life policy.

That said, there are certain unlimited financial life insurance policy policies created mainly for high early cash money worth (HECV) of over 90% in the very first year. The long-term efficiency will usually significantly delay the best-performing Infinite Banking life insurance policies. Having accessibility to that extra four figures in the first few years may come with the price of 6-figures in the future.

You really get some significant long-term benefits that aid you recoup these very early expenses and after that some. We discover that this hindered very early liquidity trouble with unlimited banking is more mental than anything else as soon as thoroughly discovered. In fact, if they definitely required every penny of the cash missing out on from their limitless financial life insurance policy in the very first few years.

Tag: unlimited banking idea In this episode, I discuss finances with Mary Jo Irmen that instructs the Infinite Banking Principle. This subject might be debatable, however I desire to obtain varied views on the program and find out regarding various methods for ranch monetary management. Some of you may agree and others won't, but Mary Jo brings an actually... With the increase of TikTok as an information-sharing platform, monetary guidance and strategies have actually found a novel method of spreading. One such approach that has been making the rounds is the boundless banking principle, or IBC for brief, gathering recommendations from celebs like rapper Waka Flocka Flame. However, while the approach is presently prominent, its origins map back to the 1980s when financial expert Nelson Nash introduced it to the world.

Within these policies, the cash value grows based upon a price established by the insurance company. As soon as a significant cash worth accumulates, insurance holders can obtain a cash money worth loan. These fundings differ from traditional ones, with life insurance policy offering as security, implying one could lose their coverage if borrowing exceedingly without appropriate cash money value to support the insurance costs.

And while the allure of these plans appears, there are innate restrictions and dangers, requiring attentive cash worth tracking. The strategy's authenticity isn't black and white. For high-net-worth people or company owner, specifically those using strategies like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and compound growth could be appealing.

Nelson Nash Bank On Yourself

The attraction of infinite banking doesn't negate its challenges: Cost: The fundamental requirement, an irreversible life insurance policy policy, is costlier than its term equivalents. Eligibility: Not everyone gets approved for whole life insurance policy because of extensive underwriting procedures that can exclude those with specific health and wellness or way of living conditions. Intricacy and threat: The intricate nature of IBC, combined with its dangers, may hinder several, especially when simpler and much less dangerous options are available.

Allocating around 10% of your regular monthly income to the plan is simply not feasible for a lot of people. Component of what you read below is merely a reiteration of what has already been claimed over.

Prior to you obtain yourself into a situation you're not prepared for, know the adhering to initially: Although the concept is frequently offered as such, you're not in fact taking a lending from yourself. If that held true, you would not have to repay it. Rather, you're borrowing from the insurer and have to settle it with rate of interest.

Some social media messages advise using cash money worth from entire life insurance coverage to pay down credit rating card financial debt. When you pay back the funding, a portion of that interest goes to the insurance coverage company.

For the first a number of years, you'll be paying off the compensation. This makes it exceptionally hard for your plan to gather value throughout this time. Unless you can pay for to pay a couple of to several hundred bucks for the following years or even more, IBC won't work for you.

Infinite Banking Simplified

Not everyone must count entirely on themselves for financial safety. If you call for life insurance, below are some useful pointers to consider: Consider term life insurance coverage. These plans give protection throughout years with significant financial responsibilities, like home loans, student finances, or when looking after kids. Make certain to look around for the finest rate.

Copyright (c) 2023, Intercom, Inc. () with Reserved Font Style Name "Montserrat". This Typeface Software program is certified under the SIL Open Up Font Style Certificate, Version 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Booked Font Call "Montserrat". This Font Software is accredited under the SIL Open Font License, Version 1.1.Avoid to major material

Bank On Yourself Plan

As a certified public accountant specializing in property investing, I've combed shoulders with the "Infinite Financial Concept" (IBC) a lot more times than I can count. I've even talked to experts on the topic. The primary draw, apart from the noticeable life insurance policy benefits, was constantly the concept of accumulating cash worth within a permanent life insurance policy plan and loaning against it.

Certain, that makes good sense. Yet truthfully, I constantly believed that cash would certainly be better invested straight on financial investments rather than funneling it with a life insurance policy Up until I discovered how IBC could be combined with an Irrevocable Life Insurance Policy Trust Fund (ILIT) to develop generational wide range. Allow's begin with the fundamentals.

Infinitive Power Bank 2000mah

When you obtain against your policy's cash money worth, there's no set settlement routine, providing you the liberty to manage the funding on your terms. On the other hand, the cash value proceeds to expand based upon the plan's assurances and dividends. This setup allows you to accessibility liquidity without interfering with the long-term growth of your policy, gave that the car loan and interest are handled intelligently.

As grandchildren are birthed and grow up, the ILIT can buy life insurance coverage policies on their lives. Family members can take car loans from the ILIT, making use of the cash money worth of the plans to money investments, begin organizations, or cover major expenditures.

A vital aspect of handling this Family members Financial institution is making use of the HEMS requirement, which stands for "Wellness, Education, Maintenance, or Assistance." This standard is frequently consisted of in depend on agreements to direct the trustee on exactly how they can disperse funds to recipients. By adhering to the HEMS standard, the trust makes sure that circulations are produced crucial requirements and long-term assistance, guarding the count on's properties while still giving for member of the family.

Raised Versatility: Unlike rigid financial institution financings, you control the repayment terms when borrowing from your very own plan. This permits you to structure payments in such a way that straightens with your organization cash money flow. universal bank unlimited check. Enhanced Money Circulation: By funding overhead through plan fundings, you can possibly free up cash that would certainly or else be tied up in typical financing payments or devices leases

He has the exact same equipment, yet has actually also constructed additional cash worth in his plan and got tax advantages. Plus, he currently has $50,000 offered in his plan to use for future opportunities or expenses. Regardless of its possible benefits, some individuals stay doubtful of the Infinite Financial Idea. Let's address a couple of usual issues: "Isn't this simply costly life insurance coverage?" While it's true that the costs for an effectively structured whole life policy might be higher than term insurance, it is very important to see it as even more than just life insurance policy.

Infinite Banking 101

It has to do with producing a flexible financing system that gives you control and supplies multiple advantages. When used strategically, it can match other financial investments and organization methods. If you're interested by the capacity of the Infinite Banking Principle for your company, below are some actions to take into consideration: Inform Yourself: Dive much deeper into the idea via trustworthy publications, workshops, or examinations with experienced experts.

{kind=link}

Latest Posts

Becoming Your Own Banker And Farming Without The Bank

Infinite Banking Concept Youtube

Cash Flow Banking Strategy